Several new opportunities were just created for land value tax (LVT) in Virginia.

Earlier this week, the General Assembly passed HB 282, which allows four more cities to voluntarily adopt a split-rate land value tax. After Governor Spanberger signs the bill into law (which passed with veto-proof majorities in both chambers), the cities of Charlottesville, Falls Church, Fredericksburg, and Newport News will obtain the legal authority to tax land at a higher rate than buildings, should they so wish.

This continues Virginia’s slow march towards land value tax (LVT), which has been taking place over the last few decades. The modern story begins with a 1998 opinion from the state Attorney General which concluded that nothing in the Virginia Constitution prohibits a split-rate LVT, but that local governments must receive explicit permission from the General Assembly before adopting one (VA is a Dillon’s Rule state). Since then, lawmakers have gradually granted that authority one jurisdiction at a time: Fairfax in 2002, Roanoke in 2003, Poquoson in 2011, and Richmond as recently as 2020.

While this one-by-one process was initially set to continue this session via separate bills for each of the candidate cities, these were ultimately combined into HB 282. Taken together, these eight cities contain roughly 7% of Virginia’s population, including two of the state’s largest cities, Richmond (population 235,000) and Newport News (185,000).

Interest in actual implementation of LVT has been building in Virginia over the last few years, particularly as the state struggles to accommodate an influx of population resulting in increasingly unaffordable housing, flooding of coastal areas, shortfalls for funding schools, and aging infrastructure.

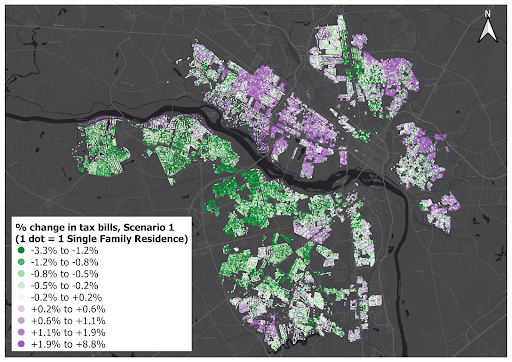

Indeed, here at PPI, we’ve published two detailed analyses of LVT for Richmond. The first, conducted on behalf of the City, found that a revenue-neutral LVT shift would be broadly progressive, tending to reduce the tax burden in neighborhoods which are lower-income. This would shift the tax burden off of multifamily housing and commercial properties, and onto low-intensity land uses such as vacant land and surface parking lots. In parallel, a series of case studies for the Realtors Association recommended implementing an LVT prior to the Richmond 300 rezoning, as a way to capture some of the windfall land value conferred upon upzoned properties. This revenue stream could be tapped to fund infrastructure necessary to accommodate growth, or to provide tax relief for the rest of the city. We have also published similar analyses for Fairfax City and Charlottesville (although the latter now relies on outdated assessment data), both of which found that a revenue-neutral LVT shift tends to reward the construction of much-needed multifamily housing, while raising taxes on vacant and underutilized land.

Recognizing the potential benefits from LVT, public officials are increasingly speaking out in favor throughout VA. Commenting on HB 282’s passage, Charlottesville Planning Commissioner Lyle Solla-Yates comments that “we have been studying tax reform measures to meet our housing, equity, and climate goals for many years now. Reducing the tax burden on Charlottesville families will provide some relief from spiking assessments while making the numbers work better for those working to protect, repair, and build the homes we need. It is heartening to know that Richmond hears us and wants to work with us to solve the problem.”

Likewise, Falls Church City Council member Justine Underhill (who also runs an urbanist YouTube channel) recently framed the issue in stark terms: “Northern Virginia is rapidly transforming from car-centric suburbs into a people-first destination, and with that comes soaring land values. And so we’re faced with a decision: should these gains translate into affordable housing and better public transit, or should they merely pad the pockets of land speculators? HB282 gives us a vital tool to ensure that this socially created value benefits the broader public.”

With the passage of HB 282, Virginia now appears perfectly poised to actually implement LVT. A meaningful set of cities now have the clear legal authority to undertake a LVT shift, with increasing interest among policymakers and advocates. This innovative tax policy can directly tackle the challenges facing the Commonwealth: by funding local infrastructure with the land value it creates, while sending exactly the right market signals to get housing built where it is most sorely needed. With eight cities now empowered to act, the race to be first is on, as the first city to adopt LVT will likely be the one to enjoy the largest gains by attracting investment in new housing, new businesses, and new jobs.